FREE RETIREMENT TALK

True Safety.

True Choice.

True Independence.

A 90-minute talk for Singapore professionals are considering their retirement, and want to understand how to integrate their CPF into retirement planning, and what true safety retirement planning actually requires.

Saturday 18 April

10am - 12pm

Singlife Building (5 Straits View, The Heart, Marina One, Singapore 018935), Level 7

FREE Live Event

What You'll Learn

Free Retirement Talk

True Safety.

True Choice.

True Independence.

A 90-minute talk for Singapore professionals are considering their retirement, and want to understand how to integrate their CPF into retirement planning, and what true safety retirement planning actually requires.

Saturday 18 April

| 🕐 10am - 12pm SGT

Singlife building (5 Straits View, #01-18/19 The Heart, Marina One, Singapore 018935)

Live Event

Limited to 30 participants

What You'll Learn

✓ How to build retirement plans that are truly safe & integrated with your CPF so your retirement finances are protected

✓ How to spot the potential gaps when speaking to Financial Agents so you know the right questions to ask

✓ What financial independence in retirement actually looks like so you can plan for it properly

This Talk Is For You If:

✓ You're approaching retirement and want to make sure your finances are truly protected

✓ You value understanding the full picture over being sold something quickly

✓ You're cautious by nature and want to know the risks before making decisions

✓ You prefer transparency and honesty over impressive-sounding promises

✓ You want to avoid mistakes that could put your retirement at risk

This Talk Is NOT For You If:

✗ You're looking for quick wins or high-risk, high-return strategies

✗ You just want someone to tell you what to buy without explanation

✗ You're not interested in understanding how things actually work

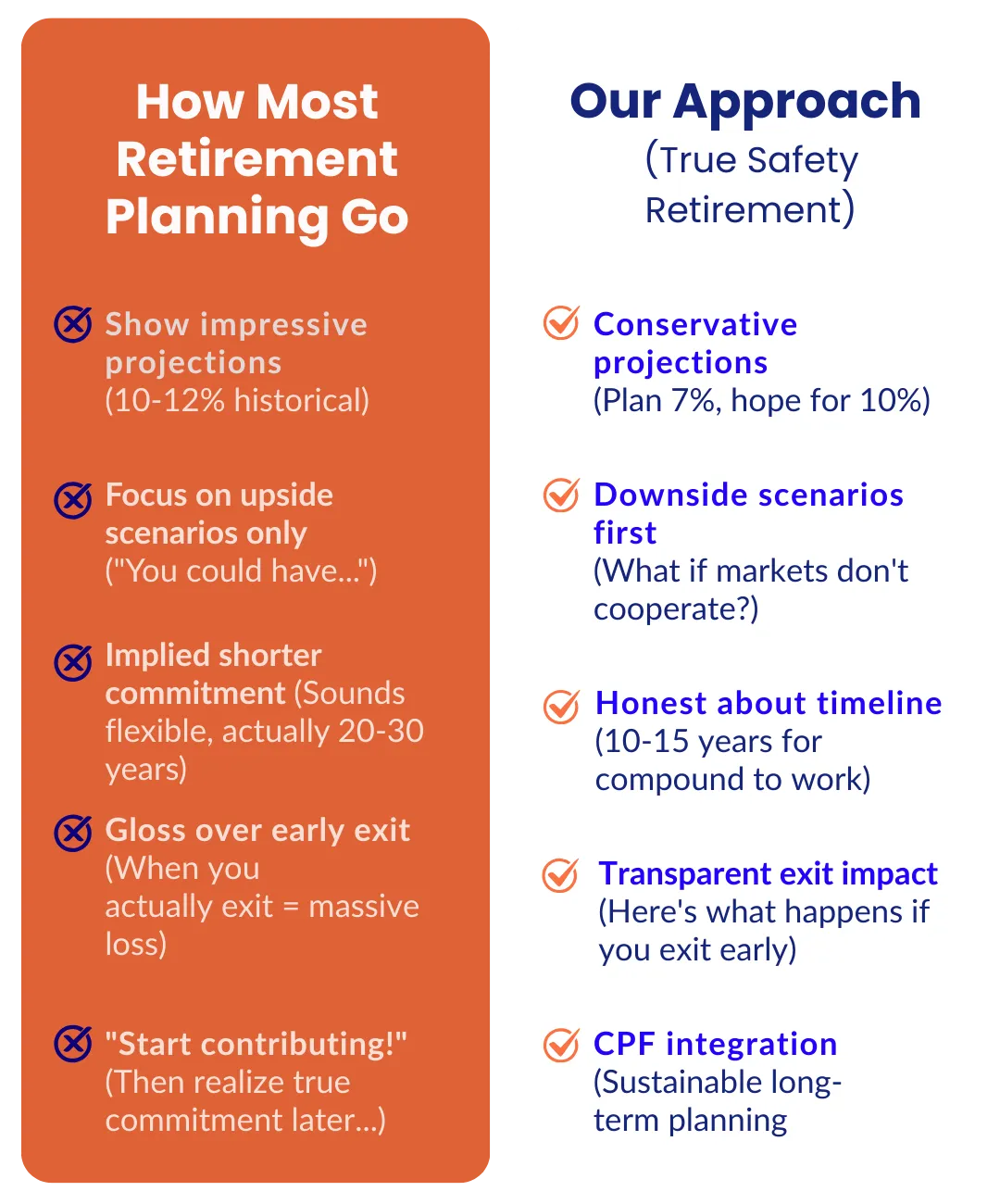

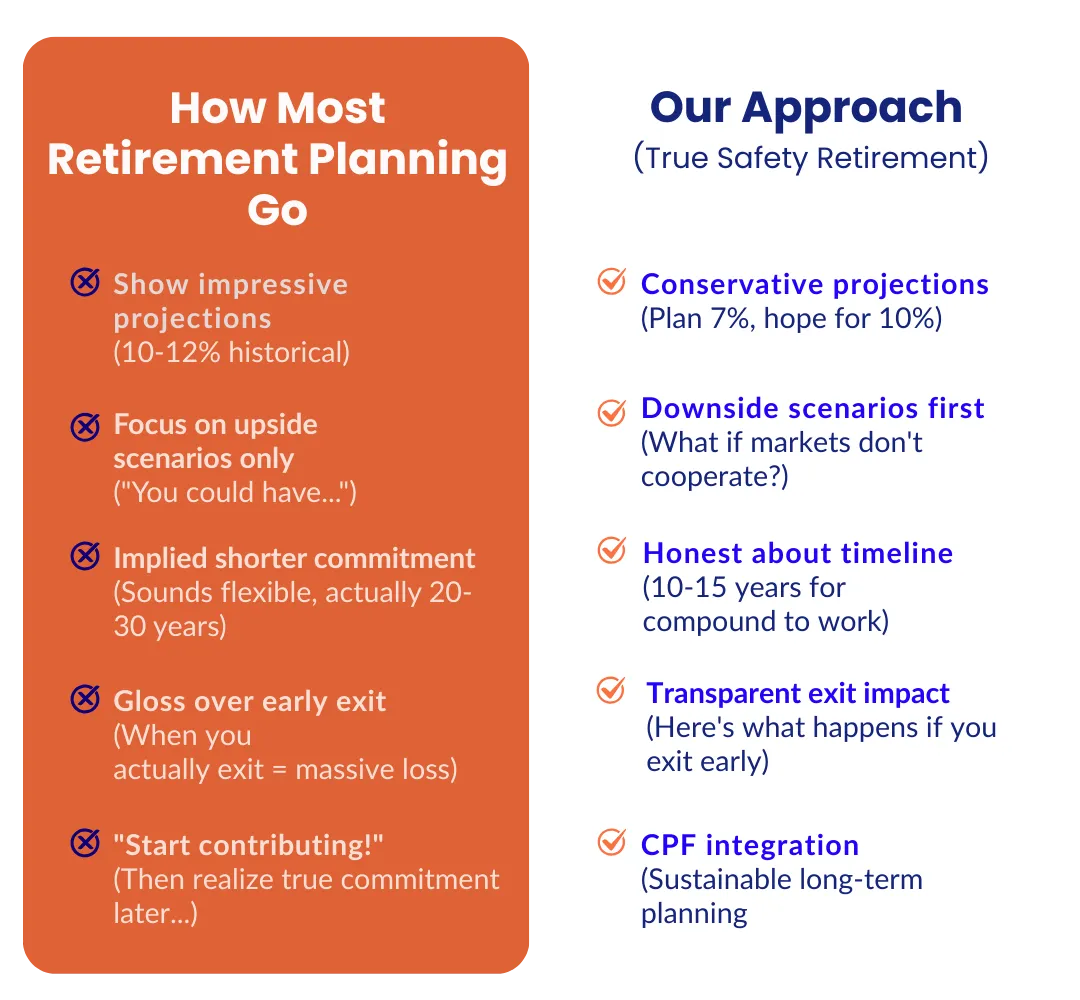

You've probably seen the ‘Retirement Planning’ presentation:

Impressive historical return projections (8%, 10%, even 12%)

Focus on the upside scenario

Presented as short-term commitment (but actually requires 20-30 years)

But here's what often gets glossed over:

What happens during market downturns? (Plan needs consistent contributions)

What if I need to exit early? (Significant loss of value when you actually exit)

How does this integrate with my CPF strategy?

The Full Picture Most Don't See

It's not that the products are bad. It's that the full picture often isn't shown:

High return focus

10-12% projections, but downside scenarios not discussed

Commitment timeline downplayed

Sounds like shorter term, actually 20-30 years

Early exit consequences buried

When you actually exit early, massive value loss

CPF integration unclear

How does this fit with your overall retirement strategy?

At this talk, you'll learn what questions to ask to get the full picture—before you commit.

What This Talk Covers

The Safety Foundation

How to build retirement plans that survive reality, not just projections

Understanding the Landscape

What drives FA recommendations and how to spot potential gaps

What Independence Actually Means

What financial freedom in retirement looks like when planned properly

Q&A at The End — Bring your questions.

Educational content only. Individual planning requires suitability assessment.

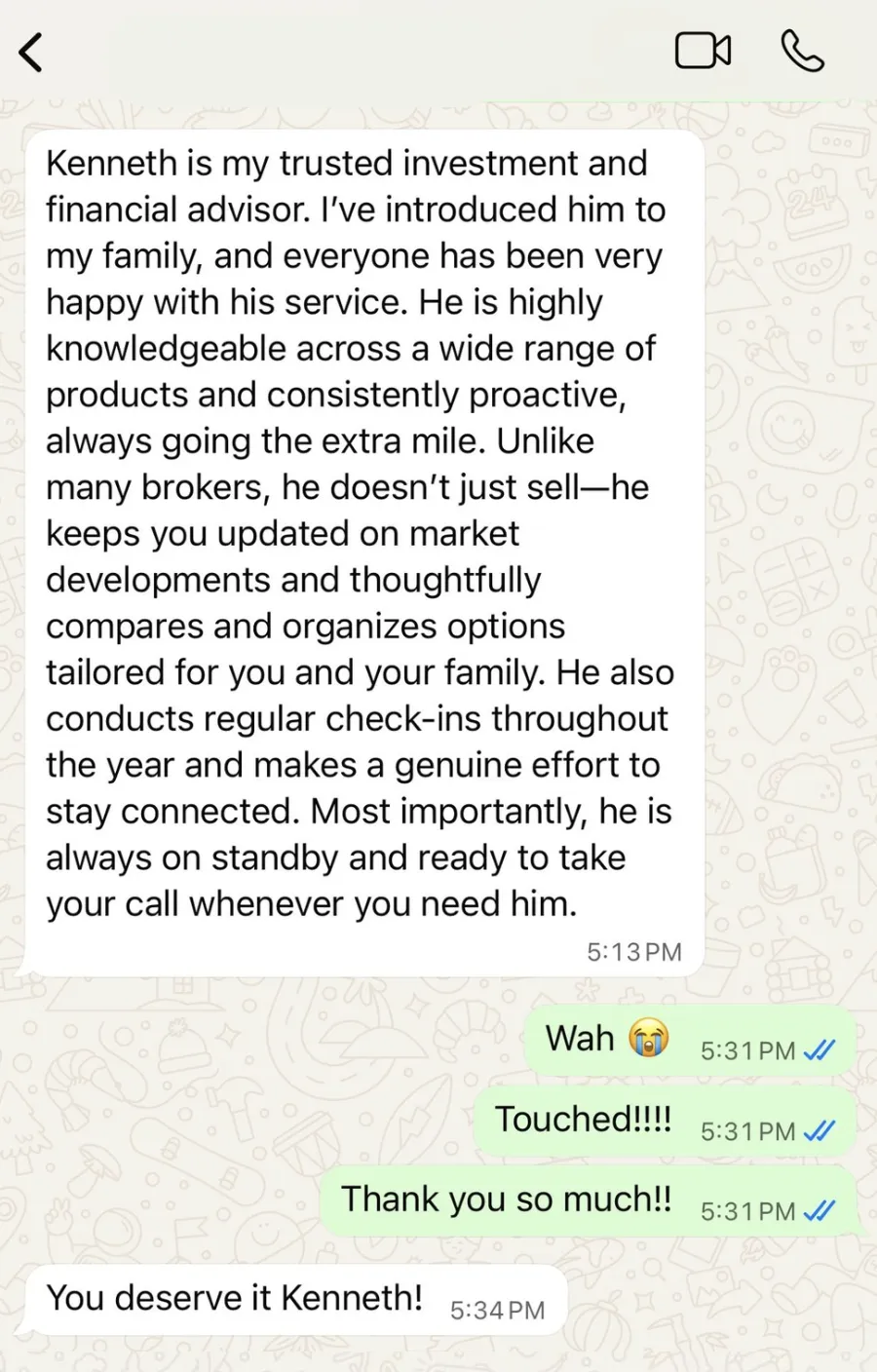

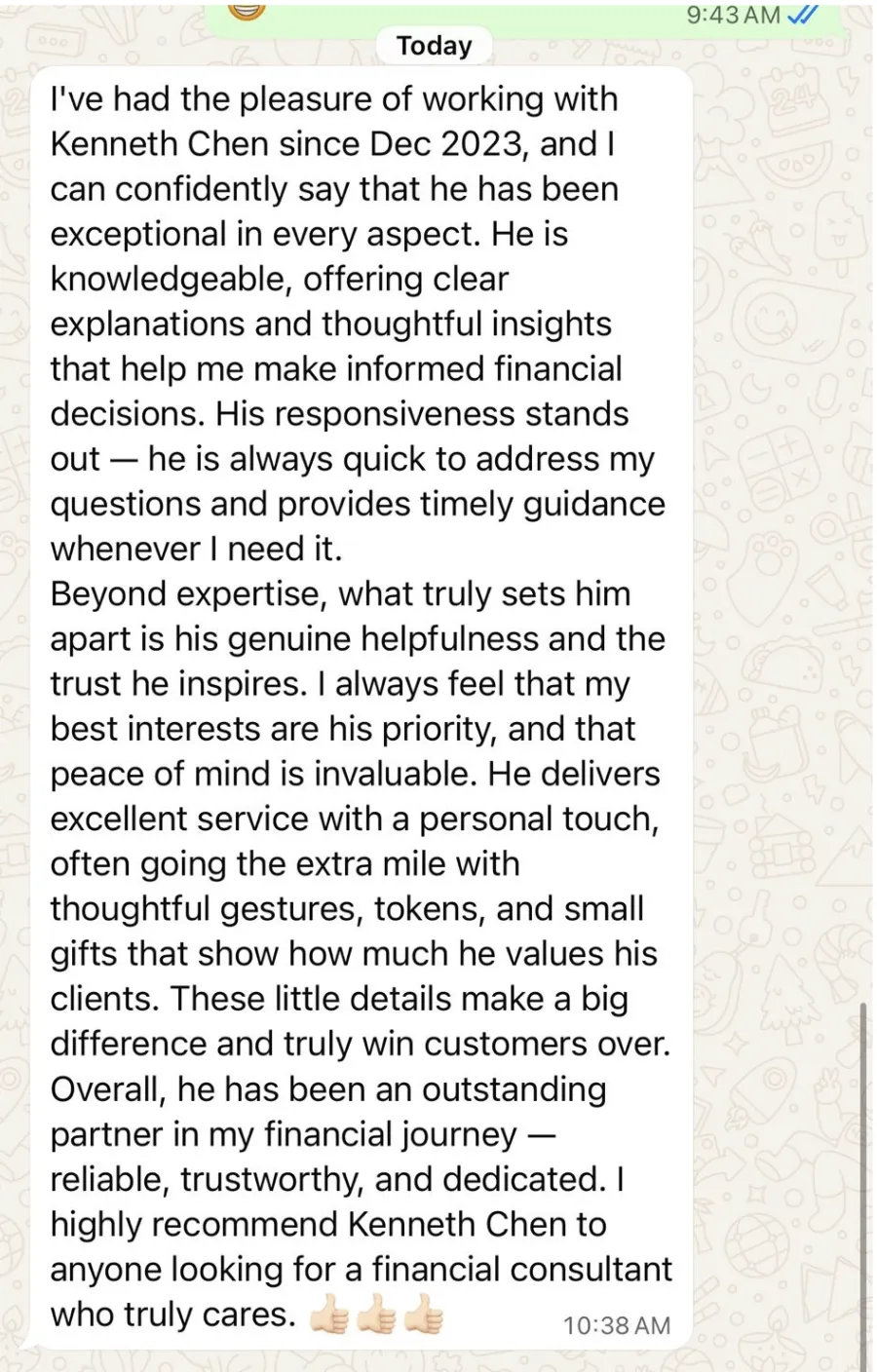

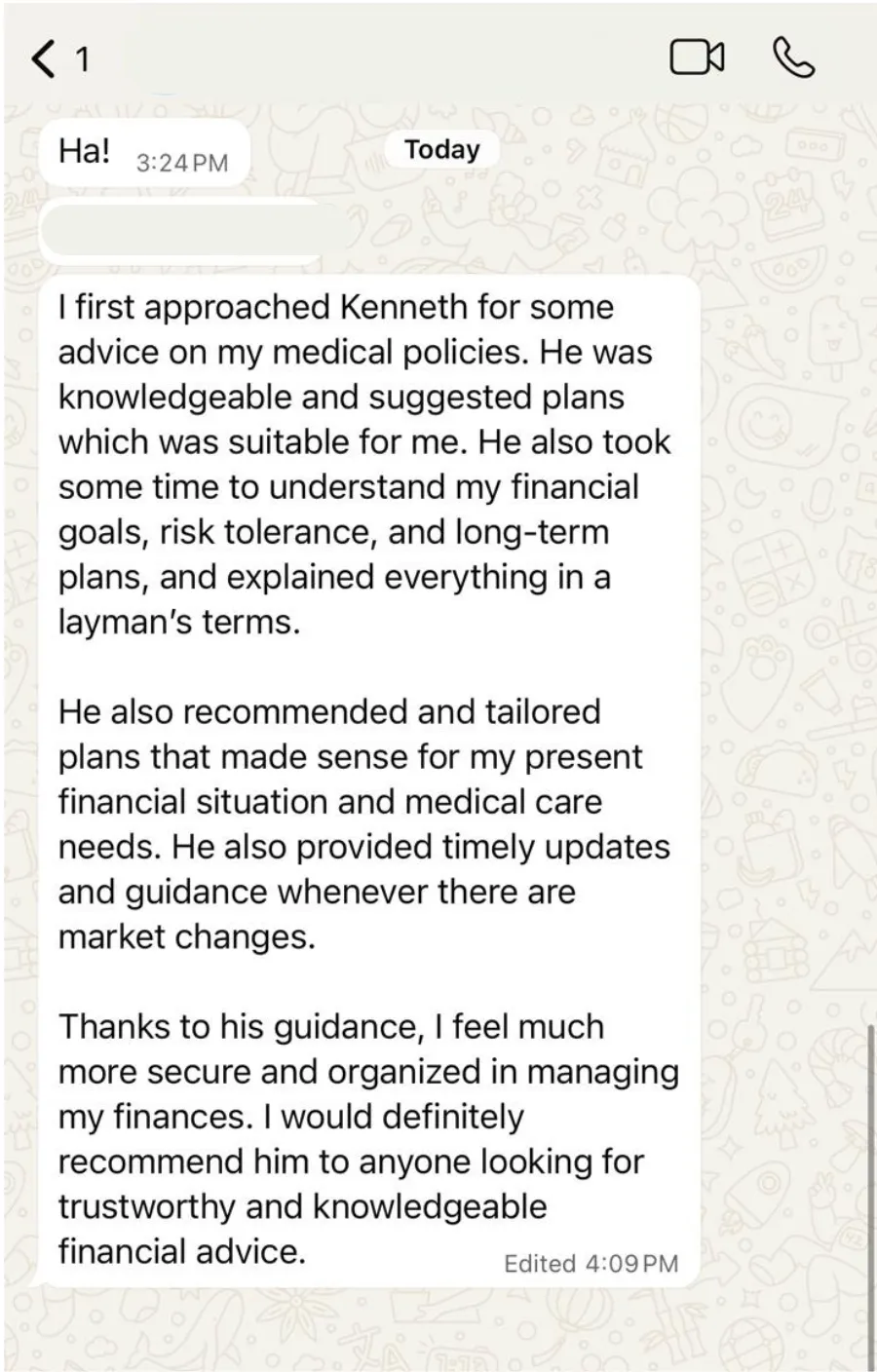

What Our Clients Say

Your Speaker

Before becoming a Financial Advisor, Kenneth was a trader.

He made S$250,000 in one night. Then lost S$250,000 in another night.

That's when he understood: crazy returns happen, but they're outliers. You can't build a retirement plan around unpredictable tail events.

"I struggled for 10 years to build something, and lost it overnight. What's the point? I don't want to take that much risk just to lose it all in one night."

So Kenneth became a Financial Advisor. But not the typical kind.

He saw how the industry worked… and he didn’t agree with it.

So he chose to become an independent financial advisor. Today, he has access to products from all major Singapore providers with the same compensation regardless of which he recommends.

His Approach:

Analytical

Shows you the numbers (Excel and all)Transparent

Full picture upfront: upside AND downsideCPF strategist

Optimizes CPF for middle-income professionals (Holistic)Mid to Long-term

Builds 10-15 year plans, not quick sales

Licensed Financial Advisor | Access to full range of products

The True Safety Framework

Real safety isn't about avoiding all risk. It's about planning so you can survive when things don't go perfectly.

The Four Components:

1. Margin of Error

Plan conservatively (assume 7%), hope for better (10%), survive downturns (5%). Never plan on best-case scenarios.

2. Avoiding Risk of Ruin

Never go to zero. The difference between losing 20% (you can recover) and losing 80% (you can't). How to structure plans that protect against catastrophic loss.

3. Compound Timeline

Why 10-15 years is necessary. Years 1-3 feel slow. Years 8-10 is where growth accelerates. What happens when you exit early.

4. Full Picture Planning

Conservative assumptions. Downside scenarios. Exit impact transparency. CPF integration. No surprises 5 years in.

This framework isn't about products. It's about how to think about retirement safety, regardless of which products you eventually use.

Past Clients

Sarah L., 48

Finance Manager

"Finally understood the early exit implications I'd overlooked."

Marcus T., 52

Civil Servant

"The commission structure explanation opened my eyes."

Jennifer K., 45,

Business Owner

First FA who showed me numbers without pushing a product.

David W., 50

Educator

"Practical frameworks I could apply immediately."

Individual feedback. Educational content only.

FAQ

Q: Any other session?

A: Session is based on availability, do sign up for a date that works for you.

Q: Will I be sold products?

A: No. Educational session only. Working together afterward is separate (and requires suitability assessment).

Q: I already have retirement planning. Still relevant?

A: Yes. You'll learn frameworks to evaluate your existing approach—particularly margin, fees, and commitment timeline.

Q: Can my spouse attend?

A: Absolutely. Register both names for accurate attendance.

Q: What age is this relevant for?

A: Most relevant for 40-55, but applicable if you're late 30s (early planning) or approaching 60 (catch-up mode).

Secure Your Seat

Learn how to build retirement plans with real safety, spot advisor bias, and understand what financial independence actually requires.

Secure Your Seat

Learn how to build retirement plans with real safety, spot advisor bias, and understand what financial independence actually requires.

Important Information

Educational Content: This session provides general education on retirement planning concepts. It is not personalized financial advice. Financial decisions should be made after assessment of individual circumstances, objectives, and risk tolerance.

Outcomes Vary: Examples and frameworks are for educational illustration. Actual results depend on market conditions, individual situations, product selection, and other factors. Past performance and projections do not guarantee future results.

Suitability Required: All financial recommendations require comprehensive suitability assessment per MAS regulations. What works for one person may not suit another.

Privacy: Registration data used for event administration and follow-up only. No third-party sharing. Opt out anytime. See Privacy Policy.